Executive Summary

- PNG has missed the opportunity to lock in potential gains to the wider economy from the successful PNG LNG project.

- The mini-boom around the PNG LNG construction phase appears to have entirely dissipated.

- PNG’s people have likely experienced their second worst recession since Independence.

- There has been at least a 10% fall in the non-LNG and non-mining parts of the PNG economy between 2014 and 2016.

- This is a conservative estimate.

- These non-resource sectors such as agriculture, retail, construction, and public services are the real parts of the economy that most matter to the people of PNG.

- There are signs of a tentative recovery with some positive recent employment figures

- Although recent lay-offs of 10% of staff by KK Kingston indicate difficulties remain.

- Based on current Treasury projected growth rates for non-resource GDP, real average incomes should return to 2013 levels by around 2022.

- Better economic policies are required to lift the long-term growth rate and ensure future resource projects are not just temporary “bumps” in lifting PNG’s sustainable standards of living.

Details

In an earlier article, I mentioned PNG’s current recession was at least 1.3% of non-resource GDP, but possibly closer to 5% once unrealistic growth figures are taken out of the agriculture sector (the official figures show strong growth in this area despite the drought in 2015).

Three sources of information since then suggest the fall has been at least 10 per cent. This information, especially tax information from MYEFO, is analysed below.

The focus in this analysis is on non-resource GDP for the reasons outlined here. Essentially, GDP growth has been dominated by the start of LNG exports, and this is in many ways a smokescreen for what was really going on for local businesses, workers, farmers and consumers.

The PNG LNG project was potentially a transformative project for PNG. There is no doubt that the project was successfully completed on time and only slightly over budget (due mainly to mismanagement of foreign exchange risks rather than other cost over-runs) and production levels have exceeded expectations. The construction phase from around 2011 to 2014 saw strong growth in sectors such as construction, wholesale and retail trade, finance, accommodation and many services. This was reflected in buoyant tax revenues and widespread employment growth. The hope was that this historic opportunity to permanently lift domestic economic activity could be locked in through the right economic policies.

Recent economic data indicates that hope has been dashed. Rather, the PNG LNG boom has proven to be just a temporary bump for the wider economy. The economy, apart from the LNG production itself, appears to have moved back to pre-PNG LNG levels. This reflects a severe recession – conservatively estimated as being equivalent to negative growth of 10 per cent.

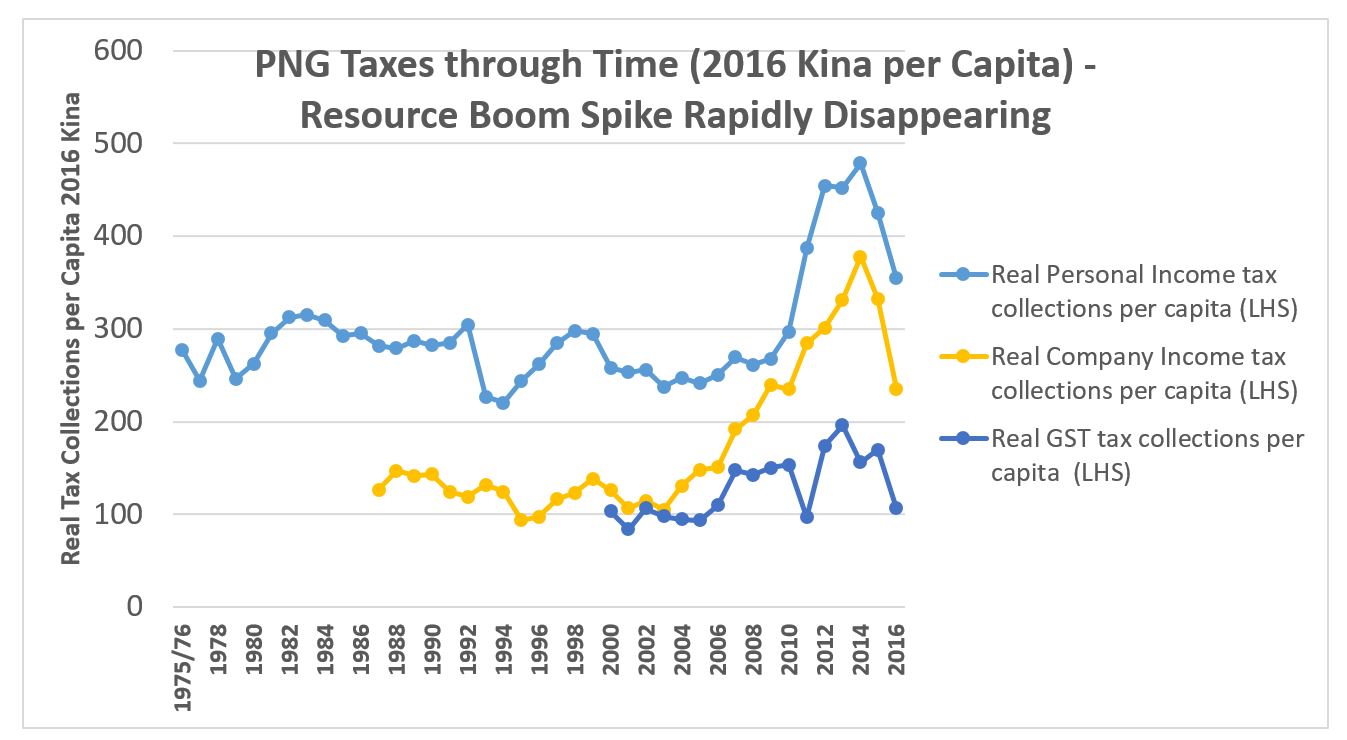

The temporary bump in economic performance from PNG LNG is reflected strongly in the pattern of tax collections.

Taxes such as personal income tax, company tax and the GST are strongly linked to underlying economic performance – such tax collections are considered to be leading economic indicators. This makes sense as personal income tax depends on the level of formal sector employment and wage levels. Company taxation is directly linked to profit levels. GST is linked to household consumption (although the figures can be affected by the timing of GST refund payments). The link between these tax levels and the underlying economy can also be affected by changes in tax policy or tax compliance but there is no evidence that these have been recent factors.

The graph below shows the real level of per capita tax collections for these three taxes (which together account for 68 per cent of PNG’s total budget revenue) .

The blue line on personal income taxes shows the average level of these taxes spiking very markedly from a level around K300 per person up to 2010 up to over K450 per person from 2012 to 2014. The most recent 2016 MYEFO figures, adjusted for a more realistic methodology (see here) indicates personal income taxes in 2016 are now estimated to be 26 per cent below 2014 levels in real terms at around K350 per person. The story on company taxes is of a marked pattern of increase following the adjustment policies from PNG’s major late 1990s recession with average real non-resource company tax levels increasing from around K100 per person to nearly K400 per person in 2014. Since then, they have dropped by an estimated 36 per cent. GST collections show a broadly similar story (except for 2011). Collections in 2016 are now estimated to be 32 per cent below 2014 levels. Combined, these three major taxes have dropped by 31 per cent in real terms.

Under normal circumstances, and with no change in policies or tax compliance, this 31 per cent fall in tax collections in real terms would suggest the economy had also declined by around 31 per cent. However, the unusual spike in such collections, especially during the PNG LNG construction phase, suggests caution in using the traditional approach.

There have been two other pieces of economic data since the first article on PNG’s recession.

Specifically, the following information on the shipping sector was provided on 4 October. “Papua New Guinea’s coastal shipping sector acts as a barometer for the country’s broader economy. While there has been a 25 per cent drop in volumes in the past year, Bismark Maritime Chief Executive Jamie Sharp tells Business Advantage PNG the market is now flattening out.” So this implies a 25% contraction that is now flattening out.

A third piece of “leading indicator” information is the report from the PNG Business Council that its members reported drops in sales of 35% in the first six months of 2016.

The combination of these three additional pieces of leading indicator information since my last blog can only point to the conclusion that the recession in PNG over the last 2 years has been at least 10 per cent of the non-resource economy. Possibly, it may be even twice as large. This would make it PNG’s second worst recession since Independence (the one starting in the late 1990s still appears more severe).

The general expectation or hope is one of flattening out – so PNG locked in at this much lower level of the economy with only slow or little growth going forward – until something changes. The most recent BPNG Monthly Economic Review provides some positive news that employment growth is slowly returning with growth of 1.7% in the March quarter and 1.4% in the June quarter (although KK Kingston’s recent decision to lay off 10% of its workforce indicates that things are still difficult). Possibly the recession is now over – but the path to restoring economic activity back to previous levels is likely to be slow.

Based on PNG Treasury projections for non-resource GDP in the 2016 budget, in per capita terms, PNG’s people will on average have to wait until around 2022 before returning to 2013 standard of living levels.

The best chance to accelerate the recovery would be to rebuild business confidence. This would require action on the exchange rate and moving away from pre-election policies in agriculture, land and SMEs that damage confidence and growth prospects. Hopefully, the proposed severe cutbacks in the budget could be backed off and more done on raising revenue. Next week’s budget will be a real test for the government in restoring some credibility around economic management.

One thought on “Recovering from recession?”

Comments are closed.