World Bank em I bin givim niupela updet long lukluk long bihaintaim bilong ikinomik bilong ol kantri insait long Saut-Ist Esia na Pasifik – lukim hia. Dispela pepa em I namba wan pepa long tupela bai I lukluk long dispela updet bilong World Bank

Stori bilong tingting long gro

Dispela stori, I luk olsem I no gutpela stori ol manmeri PNG bai I harim.

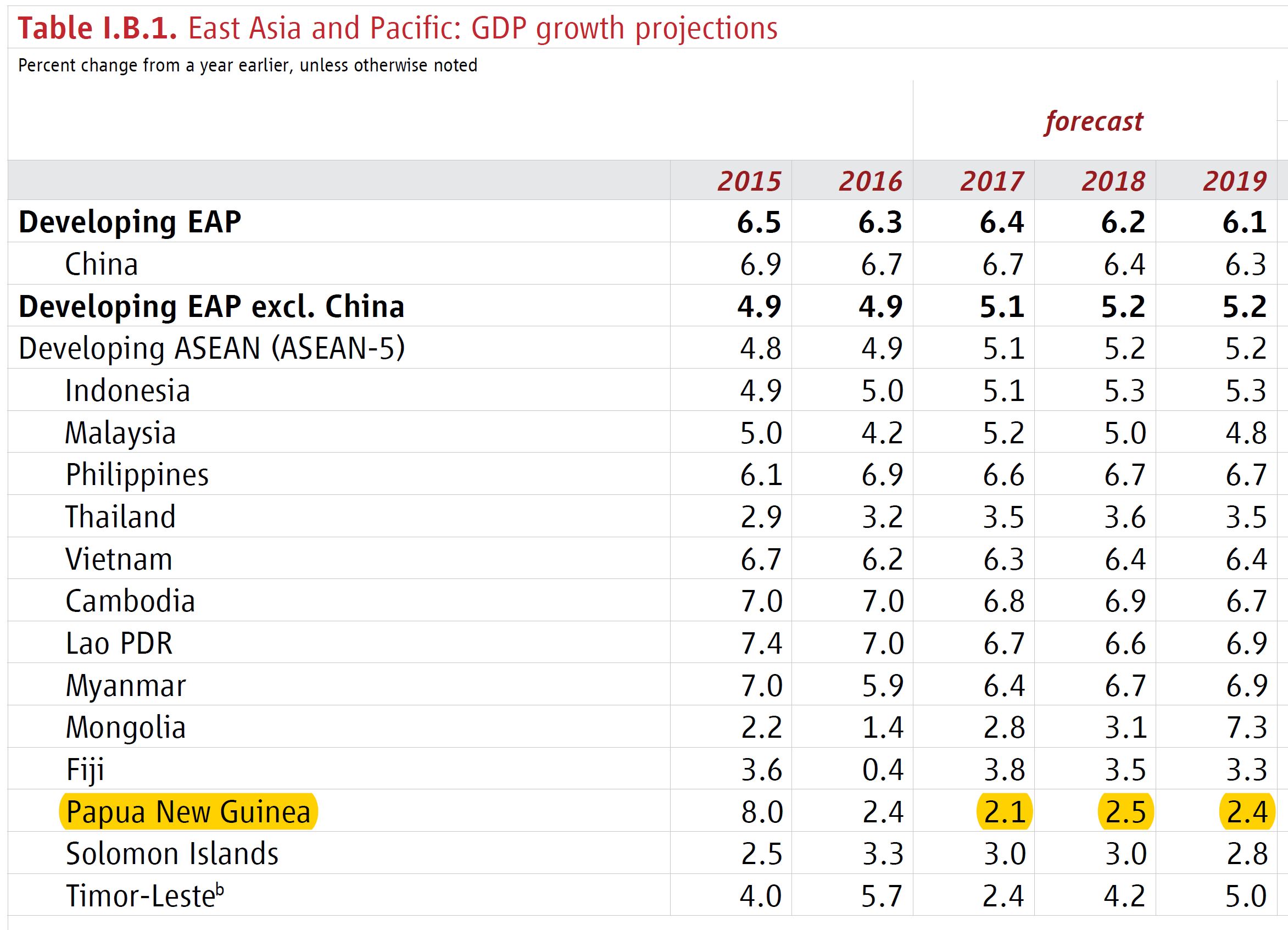

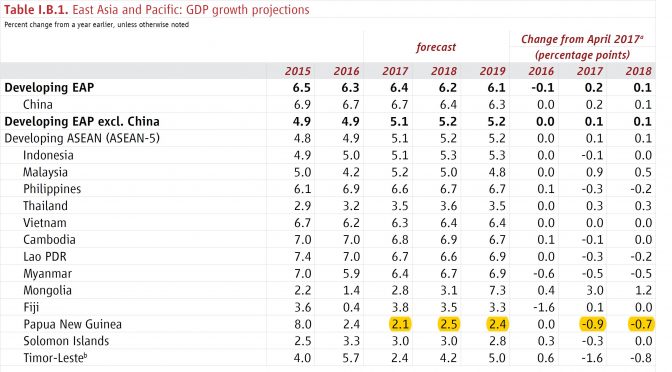

Ripot bilong World Bank I soim olsem, olgeta yia 2017 I go 2019, ol I ekspektim PNG bai kamap long las ples insait long olgeta kantri, daunbilo stret –( bai yu lukim tebol long p 30 insait long World Bank ripot. Lukim yelopela kala I soim ol namba bilong PNG I daunbilo stret. PNG bai I kam las wan stret )

Tebol I.B.1 Ist Esia na Pasifik: tingting long gro long GDP

(% senis long yia bipo)

EAP – Ist Esian kantri I wok long divelop

EAP- Ist Esian kantri I wok long divelop, tasol China I no stap insait

ASEAN – Asosiesin bilong ol kantri Saut Ist Esian

Ikonomik gro em bai 2.1 I go 2.5%, na gro bilong populesin em bai 3%, olsem ikonomik I wok long go bek, sapos yu lukim long wanwan man na meri PNG.

Las ripot World Bank i bin givim long April 2017, sixpela mun pinis. Taim yumi lukim dispela ripot na niupela ripot, yumi lukim olsem olsem, insait long niupela ripot, ol I makim gro bilong PNG I go daun long 0.9% long 2017, na go daun gen long 0.7% long 2018.

Dispela bikpela pundaun I kamap bihain long niupela O’Neil gavman I bin givim ripot long bung Alotau II , long 100-de plen bilong ol, na long Saplementari Badget.

Taim World Bank I kisim ol namba bilong PNG I go daun, ol I soim olsem ol I nogat gutpela tingting long dispel ol niupela polisi bilong niupela gavman.

Ol I tok olsem dispel “namel” gro bilong PNG insait long non-risos sekta, em I kam long sot bilong foren ekschenge, na tu olsem I kam long “fiskol konsolidesin”, olsem gavman wok long stretim hevi bilong planti mani ol I spendim na liklik mani tumas I kam insait.

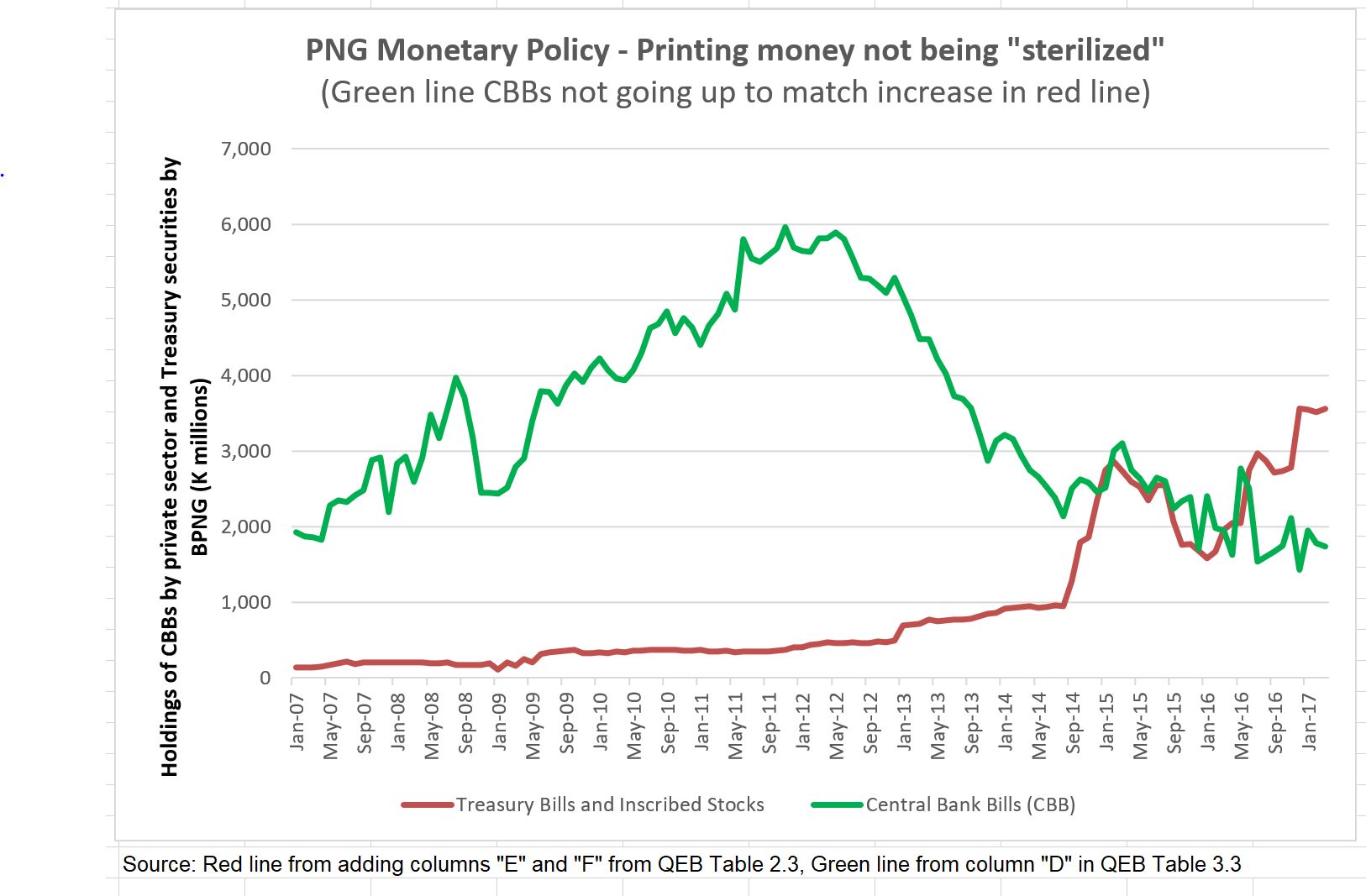

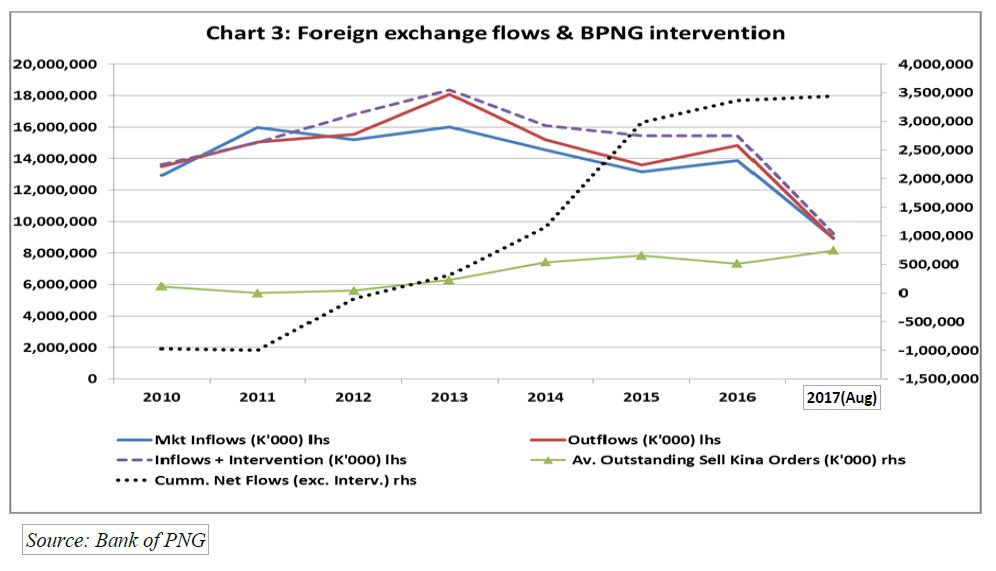

Insait long nekst blog bilong mi, bai mi lukluk long niupela BPNG Moneteri Polisi stetmen, na bai mi toktok long nogut impekt bilong ol restriksin long foren ekschange ( na tu hau BPNG I laik haitim dispela).

Wanpela narapela samting olsem, taim engin bilong gro is bagarup, inflesin tu em bai I go daun. World Bank nau I ekspektim inflesin bai I go daun long 4.1% tasol long 2017. BPNG em I tok inflesin bai I 6.0%.

2015 PNG LNG project I bin givim PNG namba wan ikonomik gro insait long Pasifik. Nau I luk olsem nogat moa gutpela win bai I givim pawa long PNG ikonomi.

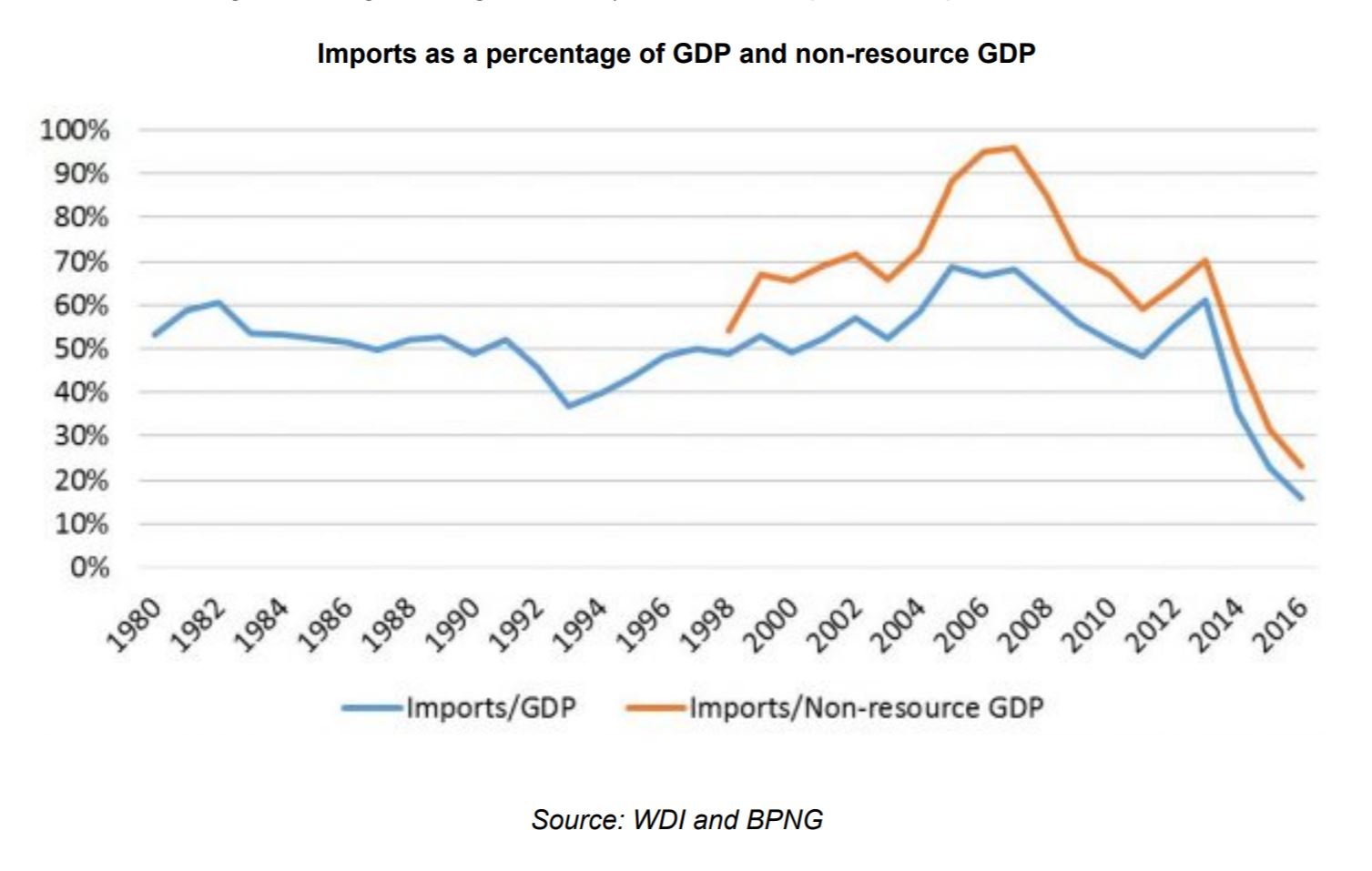

PNG ikonomi I depend tumas long risos tasol. Sapos ikonomi bai I bes long planti narapela narapela sekta, olsem agrikaltja, grona divelopmen bai I gutpela moa long olgeta man na meri PNG.

Konklusen

Yumi lukim olsem wanpela narapela referi gen bilong ikonomik, World Bank, em tu em I wari long ikonomi bilong PNG.

PNG I nidim niupela daireksin long polisi bilong ikonomik divelopmen. Wanpela artikol I bin lukim long last 40 yia na I givim sampela sadgestin – lukim long hia, na tokples Inglish long hia.

Wanpela sadgestin mi givim insait long dispela analisis, em I olsem, yumi mas sanapim ol man na meri PNG namel stret long divelopmen. Tasol I no long agrikalja o turism tasol. Wei long wokim gutpela divelopmen, em I mas bungim na lukautim ol manmeri PNG.

Ol tred na sektorol polisi nau , ol I soim olsem gavman I save lukautim ol wantok bilong em yet, tasol I no save lukautim gut olgeta manmeri PNG. Olsem eksempol bilong banis long impot – olsem PNG I bin wokim long Ramu Sugar- em I save bagarapim olgeta konsiuma. Dispela kain polisi I save bagarapim gro bilong ikonomik.

Charles Abel, niupela Tresara na depiuti Praim Minista em bai I mas makim gut wanem kain advais em bai I harim, olsem em I ken painim gutpela rot long ol manmeri PNG.

Yumi mas hopim olsem, 5 yia taim, PNG bai I gat ol namba wan namba bilong gro insait long Ist Esia-Pasifik, na ol namba bai I kam long narapela narapela sekta, I no mainim na LNG tasol.